Golar LNG ($GLNG)

Pioneer & Market leader in floating LNG vessels, with growth plans

Disclaimer: This blogpost is for informational purposes only and should not be considered personal financial advice. The author is not a licensed financial professional and will not be held liable for any decisions made based on the information provided. We simply want to take you along the journey we are making ourselves. Investing comes with inherent risks and you should perform your own research before making any investment decisions.”

Executive Summary:

Pioneer & market leader in Floating LNG vessels, giving it credibility towards all counterparties when creating new projects (1st is up & running, 2nd is almost delivered and 3rd is in the starting blocks)

Most efficient vessel design, allowing Golar to reach the lowest capex per ton floating LNG produced

Valued below book value of the vessels, while creating strong cashflows at the same time. Large part of the proceeds are hedged, although part is left open to allow for upside following the natural gas & oil commodity prices

Growth & upside potential

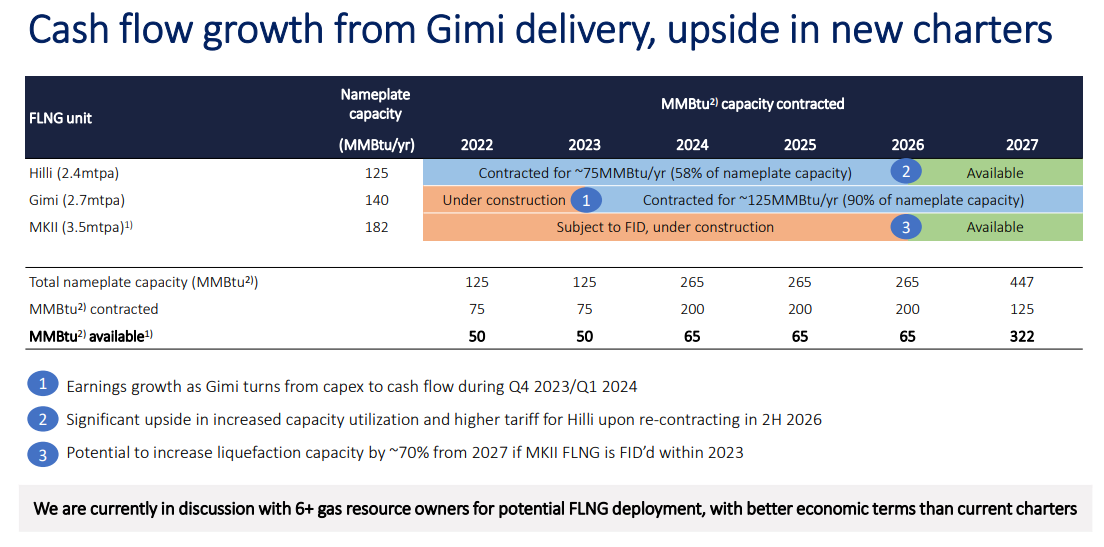

Vessel 1 - Hilli currently working at only 58% capacity → contract terms are free for redeployment as of 2026

Vessel 3 - Fuji → project in the making. Note conditions in the gas market have fundamentally shifted. When Vessel 2 - Gimi was signed, Dutch TTG gas prices were at $10-20 levels, versus the $30-50 levels today (and $300 peak during gas crisis)

Improving it’s thinking about shareholder remuneration, both through dividends & share buybacks

Only thing we don’t like is the potential concentration risk on Nigeria of 2 out of the 3 vessels are deployed there

Conclusion: Growth stock at the core of the energy transition (all mayors claiming they want to invest more in gas, less in oil). Market leader & pioneer meaning it’s the go-to company. Contains some project & commodity prices risk, hence size your position accordingly. We are buyers below $20 levels.

Analysis:

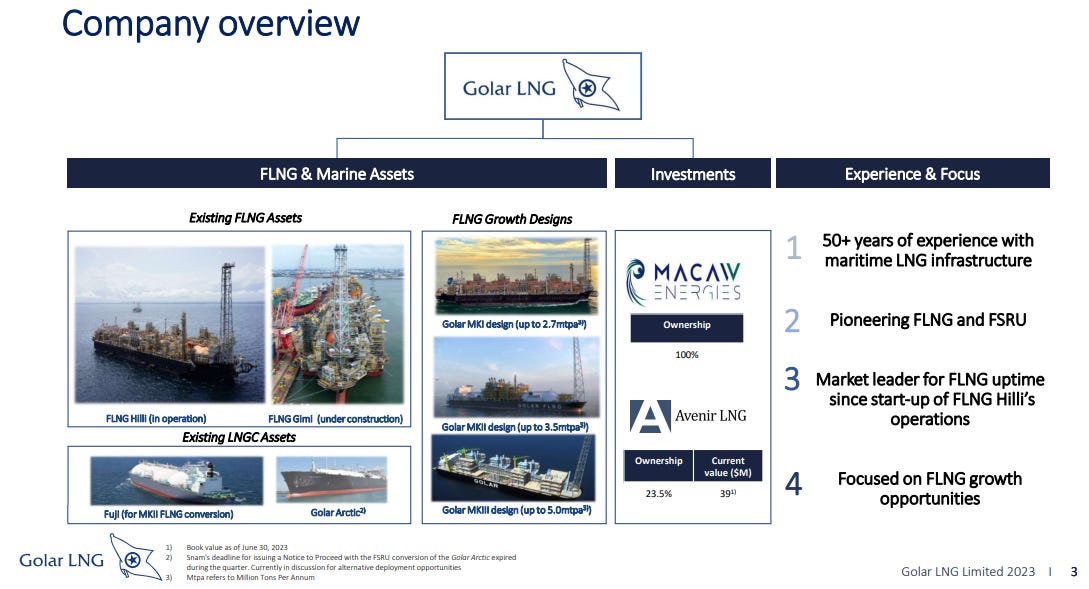

Activities & strategy

Golar is a so called ‘upstream’ company, active in the conversion of gas into Liquified Natural Gas (LNG) and thus making gas ready to transport. It is performing the liquification based on Floating LNG (FLNG) vessels.

The company used to be active in the transportation (LNG Carriers) and downstream distribution of LNG too, but recently sold all assets to focus purely on the design & operation of FLNG vessels

Currently the company has 2 vessels:

Vessel 1 - Hilli (2.4 Million Tons per Annum or mtpa)→ in operations in Cameroon and under contract with Perenco and SNH until 2026. But only used for 1.4 mtpa (i.e. 58% capacity) as their are only 4 trains (not enough wells at the time of contract initiation)

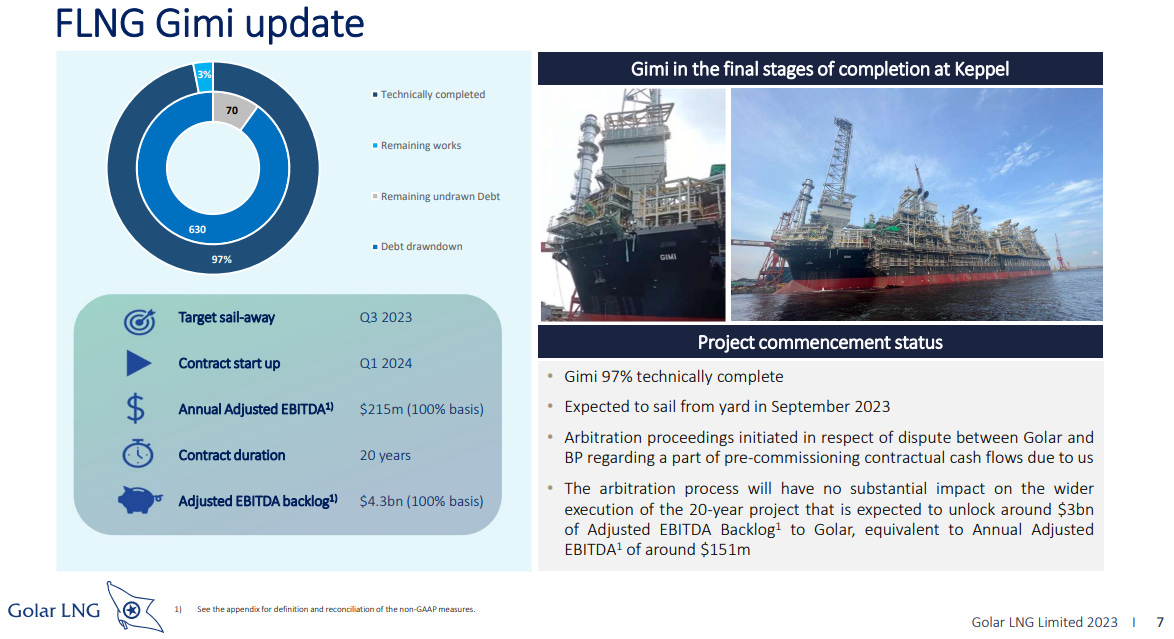

Vessel 2 - Gimi (2.7 mtpa) → 97% complete, SEP’23 expected yard departure. Will be deployed at 90% capacity in Senegal/Mauritania for BP on a 20 years contract. The project is a “copy-paste” of Vessel 1 - Hilli and is being built by the same yard

But is working to expand the fleet with a Vessel 3 - Fuji (3.5 mpta)

Exercised the option to acquire the 2004 built LNG carrier Fuji and convert it into a MKII design FLNG

Discussions with finance providers & shipyards ongoing

Discussions with Nigeria for potential deployment on a 10+ years term (and in the meantime also discussion to redeploy Vessel 1 - Hilli after the current deployment ends in 2026)

Aims to land at $ 2 bio investment, which would be approx. $570/ton showcasing the market leadership of GLNG in this domain at capex levels well below the competition

Its has a very unique and leading position in the niche of FLNG vessels. With a significant pricing advantage (lower capex) and long-time track record. If you believe that gas will play a central role in the future energy systems, GLNG 0.00%↑ is the stock for you.

CEO was closing the Q2 ‘23 results call with a hint at further news coming soon?

(thanks to

for going through all details)

Financial analysis

Incremental Free Cashflow will be generated based on

Increase in commodity prices (will not bore you with the details but part of the revenues on Vessel 1 - Hilli are unhedged + there is a bonus if oil prices are at +$60 levels)

Redeployment of Vessel 1 - Hilli in 2026 at better contract terms and higher utilization

Business development with Vessel 3 - Fuji potentially in 2026

Besides the ‘operational’ Free Cashflow, additional value can also be created from the corporate center with

Renegotiating existing debt terms (e.g. the debt for Vessel 1 - Hilli was prolonged and repriced with a lower margin)

We refer to a previous valuation made by Jacob Rubin (Philosophy Capital)

Vessel 1 - Hilli is worth $13/share (despite lower utilization, its the upside for higher commodity prices that gives the higher valuation)

Vessel 2 - Gimi is worth $9/share

Any additional Vessel is a bonus to the existing share price

Another way to look at valuation is purely based on the value of its assets. For example, the FLNG Vessel - Tango, built by Exmar with 0.5 mtpa was sold to ENI for $570-690m (depending on its performance).

Applying the same ratio to GLNG’s two vessels with give a rough $5b asset value, to be diminished with its current $0.2b net debt outstanding.

As mentioned this is a very rough ballpark number, as Tango was a newly built vessel, while Vessel 1 - Hilli is already in use and might need some refurbishment / have a shorter lifespan. But in comparison with the current market cap of $2.5b (at $22/share) it shows GLNG has some room to grow.

The company recently started to think about shareholder return through

Quarterly dividends - currently at $0.25 / share / quarter

Repurchase a first batch of shares at $21 for $30m, and still has $120m of approved capacity remaining

Mgmt indicated they received several unsolicited offers to take the company private at a premium, but considers the company value to be higher more after completion of the current projects running (e.g. redeployment of Vessel 1 - Hilli and start of construction Vessel 3 - Fuji)

People

Current management is fairly new and can be considered the main executor of Golar’s focus on FLNG vessels and recent strategic focus

CEO Karl Staubo was appointed CEO on May’21 and was CFO the year before. Before joining Golar, he spent 10 years advising and investing in Shipping, with Magni Partners Ltd. (2018-2020) and Clarksons Platou Securities (2010-2018). At Clarksons Platou Securities he worked in the Corporate Finance division, including as Head of Shipping, Investment Banking (2015-2018).

CFO Eduardo Marahão was appointed at the same time as Karl. Prior to becoming CFO of Golar LNG, he served as CFO of former affiliate company Hygo and as a partner at Magni Partners (as did CEO Karl Staubo). Mr. Maranhão has vast experience in international energy projects and infrastructure financing having worked at different financial institutions including Lakeshore Partners, Santander, Credit Agricole, Banco Votorantim and Citibank. Mr. Maranhão holds a Bachelor of Business Administration from Universidade de Pernambuco in Brazil and has completed a Management Acceleration Programme from INSEAD in France.

Shareholders

There are few key shareholders. From the 106m shares outstanding,

5.6m are owned by the Sohmen Pao family, which controls Hong Kong's World Wide Shipping Group, founded by the legendary Sir Y.K. Pao

5.6m are owned by Tor Olav Trøim, former CEO and current Chairman

The biggest position by investments funds is taken by Orbis Investment Management Ltd. with 9.5m shares

Note there is no management ownership