Energy SpA ($ENY.MI)

EU small cap at reasonable valuation with strong ties to Chinese supplier in a fast growing energy market

Conclusion:

Ownership spread over founders/mngrs and long term shareholders. Recent 2022 IPO proceeds (€27m) were used to grow the company, not for shareholder exit. 20% dilution though if financial results are reached.

High growth company in residential Energy Storage Systems, and already profitable for +4 years. Thanks to this, Energy SpA was able to self-fund its growth for a long time.

Outlook seems conservative (Energy SpA overachieved +30% growth in recent years). But this was based on residential sales. Italy subsidy regime stopping and company wants to shift to EU & USA sales and more large systems. To be seen if it can reach its targets (larger system sales = lower margin & higher capital consumption?). Inventory up, and sales backlog down does not point in the right direction

With its ‘22-’24 business plan, current valuation is only 5x EBITDA and 7,5x P/E. This leaves a buffer for disappointments, and lots of potential upside

(e.g. competitor Enersys at 10x EBITDA and 25x P/E)

(e.g. supplier / JV partner Pylontech at 111x EBITDA and 51x P/E)(e.g. competitors Fluence Energy & Stem at negative EBITDA and negative Earnings)

Strong balance sheet position with only €8m net debt vs €32m EBITDA. Allows for faster growth than 30%/year (and cash will be consumed for working capital) or allows for acquisitions (would prefer not to, as higher risk). High inventory, but assuming this is not ‘perishable’ and battery components can be used indifferently in small or large systems.

Currently a small market cap (€170m at €3,5/share), but the bigger it becomes, the more ESG funds will invest in the company. This will drive ‘multiple expansion’ to higher P/E and EBITDA multiple levels.

Future capital increases could be expected given such high growth rate, but will probably be done at higher & higher valuations, as the company will be able to prove its growth & profitability track record.

Actions: set a limit buy order at €3 / share to capture some small cap volatility

Next steps: 27 SEP 2023 half year results presentation

Thanks to @SharogradskyM for making me curious

Analysis:

Activities:

Founded in 2013

Sells Energy Storage Systems (ESS) such as batteries, inverters, … integrated with proprietary management software (chose when to charge your vehicle, peak shaving, … this will grow in importance as current grid is not capable to handle energy peaks).

Does not sell to the end consumer. Sells to distributors (PV installators, energy grid companies) both branded and white labeled. Trying to establish a direct sales link with large Engineering, Procurement & Construction (EPC) companies who design large renewable energy plants directly.

Primary market is Italy residential consumer (boosted by local subsidies - which don’t need to continue to allow reaching their future business plan). Looking to expand growth by going after larger projects & cross-border sales.

Announced JV with Pylontech in FEB 2023 (Chinese $6,6b world leader in Lithium batteries - Top 2 supplier in residential batteries - $56m EBITDA - strong balance sheet with 75% equity - doubling production capacity every year) . This Italian JV with €10m investment is important as:

It guarantees Energy SpA of a supply of batteries while demand volume grows rapidly. It can provide guarantees of delivery to its (potential) customers.

Allows Energy SpA to claim part of the cake in selling batteries in EU

(JV is 70% Pylontech + 30% Energy SpA) instead of simply importing & reselling Pylontech batteries.It will start producing ‘Made in Italy’ batteries, countering the potential ‘Made in China’ risks (e.g. necessary for subsidies?)

Markets its products under the ‘zeroCO2’ brand

Batteries are Lithium-Iron-Phosphate (LFP) and are Cobalt-free (important for ESG accreditation - contrary to regular Lithium batteries)

TO DO - read up on batteries technology

Website is not top notch … E.g. reference page is blanc, no real ‘buy now’ buttons

It seems to be more focused on the investor, than on a potential client/distributor. On the other hand, the company is not going for direct sales (in the small ESS market - but what if they want to grow direct Extra Large sales?). Feels like they have some work to do if they want to compete with Stem / Fluence Energy on US soil (and capture some Inflation Reduction Act dollars).Moving to a full system integrator

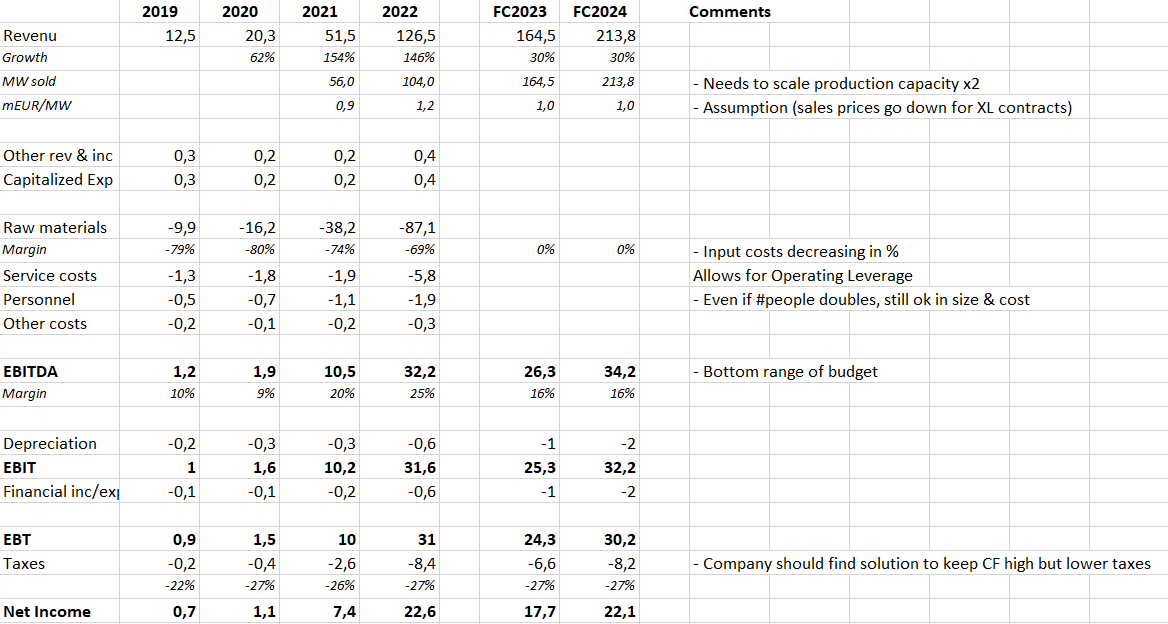

Financial Accounts:

Almost no expenses capitalized on the balance sheet. All R&D straight into expenses of the year and still making a nice margin

Large amount of income taxes, cashflows can be optimized further utilizing the debt tax shield better (if working capital needs stabilize)

Most of debt is used for working capital. Inventory build up from €7m FY21 to €60m FY22. Going after large contracts is not good for working capital needs.

Biggest expenses are raw materials to build/buy the batteries, not labor

Simple financial accounts, no tricks or creative accounting

Nice gross margin / high ROE (up until now, large contracts generally have lower margins + large contracts require large working capital which decrease ROE)

Backlog drying up?

€43,8m reported at 1H 2022 results, dropped to €26m at year end 2022

Competition (Fluence / Stem)

Fluence → buys batteries from AES & Siemens

Stem → started as solar installation company, now sells solar + batteries 50/50

Both have a very large orderbook (multiple times annual revenue)

Play in the ‘big league’ aiming for mega installations

However this is not where the fat profit margins are found, both companies have negative earnings & EBITDA (despite 10x the size of Energy SpA)

Fluence → 900 MW ESS deployed in FY2022 vs $1.180m revenue = 1,3 mUSD/MW charged, which is in line with Energy SpA. Hence their lower Net Income should be due to (1) higher purchase prices and (2) larger/inefficient operations

Inventory doubled for Fluence at Dec 2022 ($652m → $1.083m)

Shareholders

11m shares (or +20%) dilution in next years, dependent on financial results

Managers & Co-founders Tinazzi & Taffurelli have background in Mitsubishi Electric Klimat Transportation (air conditioning producer for rail & tram)

Euroguarco = Ghirlanda family holding containing several internal developed business units that specialize in supply of sealing products and insulating materials to the production of valves, piping products, engineering and fabrication of skid packages, engineering and manufacturing of systems of ducts, wallheads and interiors for trains and ships. No financials found

Sun Hongwu = Chinese business woman introducing the IT owners to the Chinese market. (Explanation provided by Energy SpA, no extra info found online)