Cofinimmo ($COFB.BR)

Sector under stress, but best positioned compared to peers to deliver value

Conclusion:

Main focus is healthcare properties (72% portfolio) where the stress is on the operators (e.g. Orpea in FR, Curata in DE), not the property. The biggest risk would be renegotiations on the rents with some mayor operators, but this will surely not suddenly half the rental income ? Cofinimmo has low exposure to the worst operators and a well spread portfolio.

Cost of debt is hedged for the next 5 years, who knows where interest rates will be then (and rental income will have inflated further for this period)

Trading at a 40% discount to Net Asset Value (if you would sell all properties today at their fair value). Recent sales of office buildings are confirming this valuation.

The sector is in a bad place with competitors going for equity increases at record low share prices (e.g. Aedifica). Cofinimmo has a EUR 300m investment plan for 2023, and will realize it by selling existing Office spaces (already EUR 190m signed)

=> We like the discount to NAV and the dividend yield (almost 10% gross) and will take a first position around EUR 66,66 per share. We keep an eye on the healthcare operators (i.e. Cofinimmo’s renters) and will increase/decrease this position on further news about their financials

Analysis:

Strategy

Invest in Healthcare property in Europe, with the benefit of having a longer lease term (+15 years) and a high occupation ratio (100%)

Divest old portfolio of Office property. And for the Offices Cofinimmo decided to keep, they prefer stability in tenants (Public sector exposure is growing, with a higher lease term and thus stability, at the cost of a slightly lower yield)

Financials

Rather simple set of financials:

Rent comes in (approx EUR 320m on yearly basis), and evolves with inflation rate

Expenses (approx. EUR 100m) go out, linked to general operations and financing

160 FTE managing all sites - giving EUR 65m expenses

45% debt ratio - giving EUR 25m interest expenses

and EUR 10m taxes

The remaining EUR 220m cash can be distributed over the 32.8m shares, with a payout ratio of 90% (i.e. EUR 6.20 dividend per share)

Risks for the future

Rental income could be under pressure, given healthcare operators face a hard time (main expenses are wages & heating, which are pushed upwards by inflation). But Cofinimmo has a nicely balanced portfolio

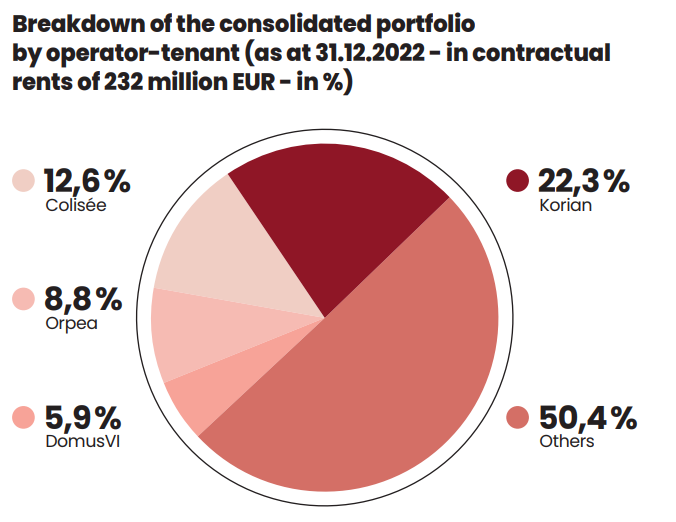

*note on FR* Orpea represents only 6.1 % of Cofinimmo’s rental income at FY2022 (Belgium 2.5 %, France 1.5 %). Orpea announced to close 10 sites in Belgium, but only 2 sites are with Cofinimmo (Aedifica is more hit).

*Note on DE* Two care home operators, Curata and Convivo, filed for insolvency. Cofinimmo’s exposure to these is very limited (respectively less than 0.2 % and less than 1 % of the contractual rents

→ Even if rents are renegotiated, lets say the full portfolio gets a 10% haircut, which is EUR 32m less income

Financing costs are higher in the current environment. Luckily Cofinimmo hedged itself (low cost of debt at 1.4%) and has a high average debt maturity of 5 years

*Note* Most of the debt is eligible under an ESG label, helping to lower interest costs

→ Say cost of debt goes back to 4%, on current EUR 3b debt, that would be a whopping EUR 78m extra interest. No wonder markets are nervous. But 83% of it is hedged for the next 5 years, leaving the immediate risk only at EUR 13m.

If rents were to appreciate with 2% inflation for the next 5 years, income will be EUR 33m higher again, compensating almost 75% of the above negative effects

Competitors like Aedifica have invested heavily last years in new properties and need to deliver on their programs. Hence they approach the market with capital increases at the moment as solution of last resort (if not, the debt ratio would increase, leaving a debt snowball eat away available dividends and also lowering the share price without the benefit of having done a capital raise). Cofinimmo is not in that tight spot, as the investment program for 2023 is covered by selling Offices in portfolio. There does not seem to be a need to go to market (EUR 190m of the EUR 300m program is already covered)

Discount to Net Asset Value

When taking all properties, assigning a ‘Fair Value’ to them based on a Discounted Cashflow Model, Cofinimmo estimates it should be worth at least EUR 108/share. Which is a nice 40% discount versus todays share price at EUR 67.

Granted, it is still a modelled approach, but we should take into account

The cashflows here are rental income, which is more stable than a normal business plan cashflow

The recent Office building sales were all done at or above this Fair Value, indicating the model did not provide an overestimation

Comparison to peer Aedifica ($AED.BR)

Both companies are listed on the Brussels Stock Exchange and have a similar profile (e.g. focus on Healthcare Real Estate, approximately EUR 6b balance sheet, active all over Europe but grown from their core activities in Belgium).

However, in our opinion the recent all-time low in the share price of Aedifica is dragging Cofinimmo along

Aedifica grew faster in the past low-interest rate environment years (e.g. EUR 800m projects were delivered in 2022). Given their pure play on Healthcare, the acquired properties with an average lease term that is very long (avg lease term +19 years) hence locking-in the lower rental income yield for a longer time (gross yield is 5.5%)

Aedifica has a larger exposure to the UK market, which is currently more stressed (higher BoE rates, higher inflation putting pressure on local nursing operators). Note also that indexation of rents on UK healthcare is generally based on the retail price index with contractual floors and caps

Exposure to the French operator Orpea is larger than Cofinimmo. The Orpea group operates in 21 Aedifica care homes (BE: 9; DE: 5; NL: 7) and represents 4.8% of the contractual rental income (BE: 2.5%; DE: 1.2%; NL: 1.1%). As part of Orpea’s strategic transformation, it no longer considers Belgium as a strategic market and intends to stop operational activities in five Aedifica care homes

The debt structure is also more prone to interest rate increases, as refinancing will be needed for some substantial bonds in the following years, plus they were not fully hedged towards an interest rate increase

From Aedifica Annual Report: On 31 December 2022: - approx. €423 million in long-term debt will mature within one year, €265 million in 2024 and €170 million in 2025; - 66% of the Group’s financial debt consists of floating-rate debt and 34% of fixed-rate debt. The unhedged part of the total financial debt equals 22%.

The company has substantial investment commitments in the following years. There is a EUR 670m pipeline of projects (pre-let developments + acquisitions) which cannot be covered with additional debt, nor with optional dividends (i.e. giving shares instead of cash, keeping the cash in the company). Hence their recent choice to launch a EUR 380m capital increase at EUR 52/share (which was an initial 13% discount when announced)